M&A and Joint

Venture Activity

Volume Strengthens in the

Wake of Mega-Deals

M&A and Joint

Venture Activity

Volume Strengthens

in the Wake of

Mega-Deals

If 2023 was characterized by a small number of mega-deals that reshaped the top end of the U.S. oil & gas industry, 2024 was about post-consolidation deal flow and a steady uptick in activity across the market. In the run-up to the U.S. election in November, we saw a lot of transactions being discussed but not executed, foretelling what we expect to be a busy year for our clients in 2025.

Strategic M&A

Divestments Fuel Volume

Pickup Going into 2025

M&A activity looks set to take on a different tone this year as major consolidation plays bed down.

Global M&A Value Up Following Mega-Deals

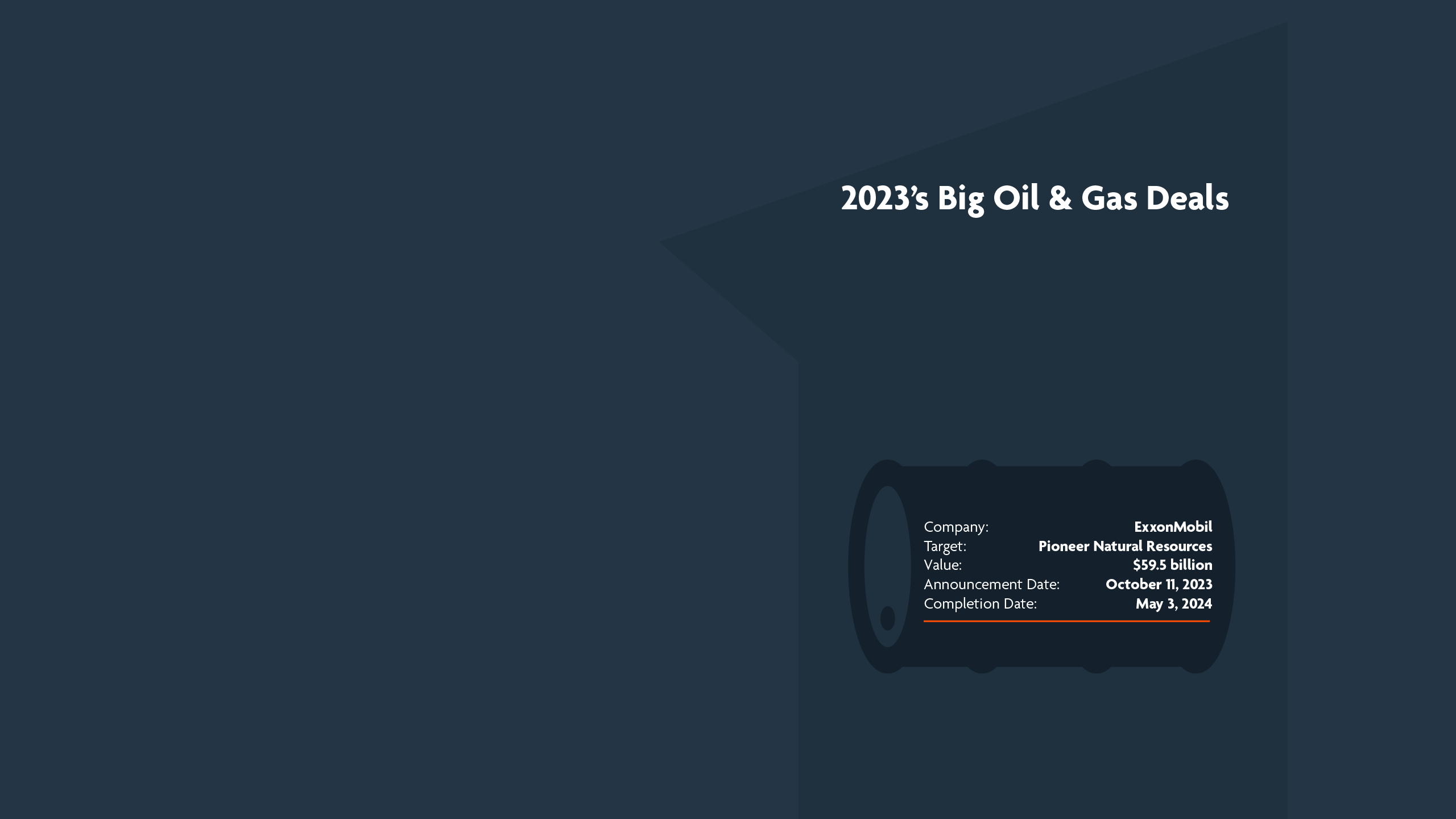

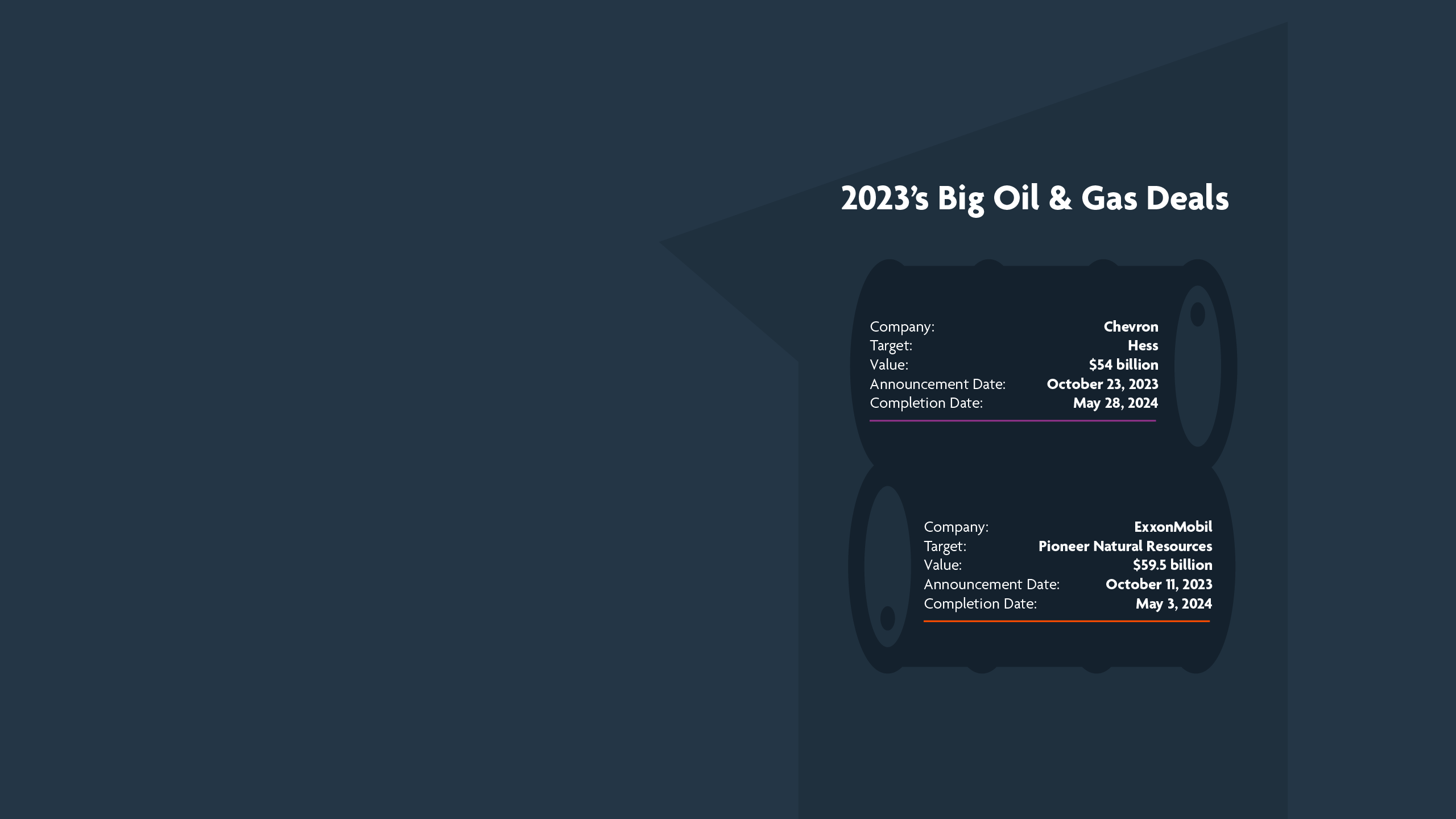

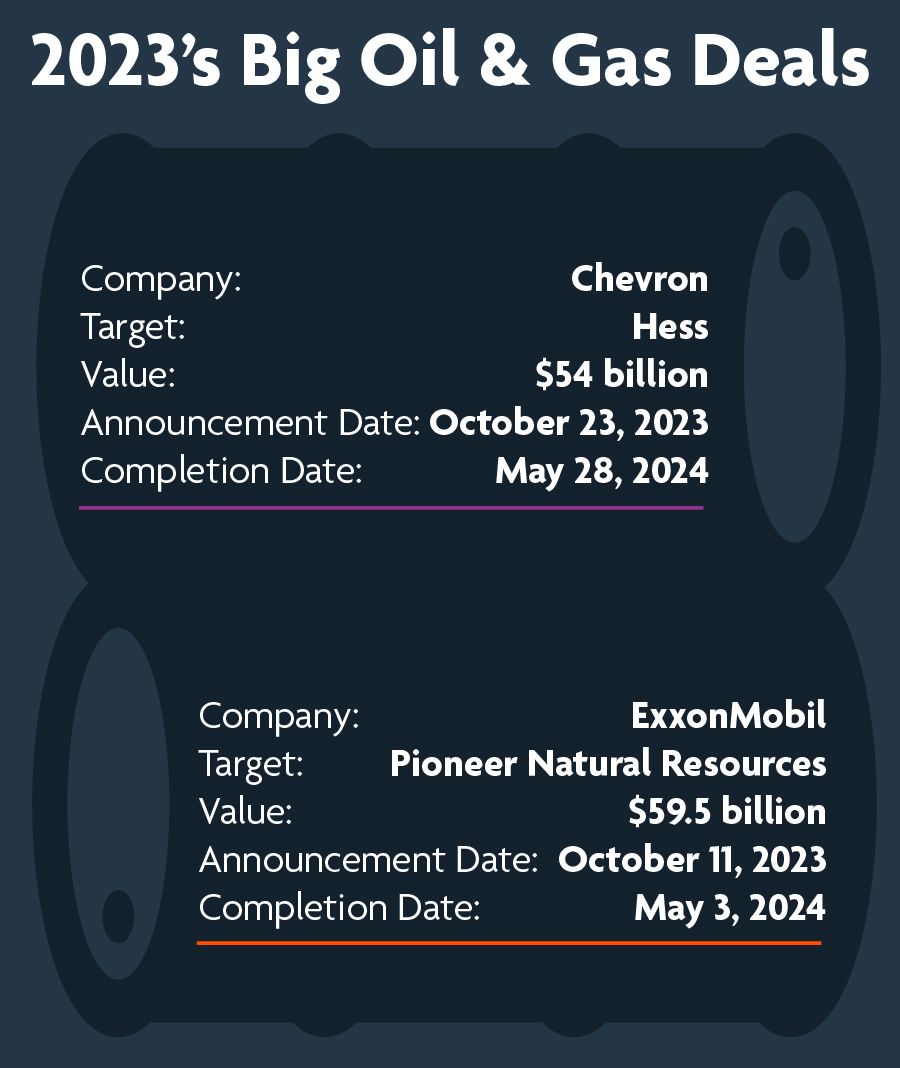

As 2023 came to a close, the U.S. oil & gas markets were shaken by two big deals that would go on to define that year: ExxonMobil, the largest U.S. oil producer, announced its agreement to buy Pioneer Natural Resources for $59.5 billion in October to create the biggest producer in the Permian Basin, and soon after we saw Chevron reveal plans to acquire rival Hess for $53 billion.

If 2023 was characterized by a small number of mega-deals that reshaped the top end of the U.S. oil & gas industry, 2024 was about post-consolidation deal flow and a steady uptick in activity across the market. In the run-up to the U.S. election in November, we saw a lot of transactions being discussed but not executed, foretelling what we expect to be a busy year for our clients in 2025.

Strategic M&A

Divestments Fuel Volume

Pickup Going into 2025

M&A activity looks set to take on a different tone this year as major consolidation plays bed down.

Global M&A Value Up Following Mega-Deals

As 2023 came to a close, the U.S. oil & gas markets were shaken by two big deals that would go on to define that year: ExxonMobil, the largest U.S. oil producer, announced its agreement to buy Pioneer Natural Resources for $59.5 billion in October to create the biggest producer in the Permian Basin, and soon after we saw Chevron reveal plans to acquire rival Hess for $53 billion.

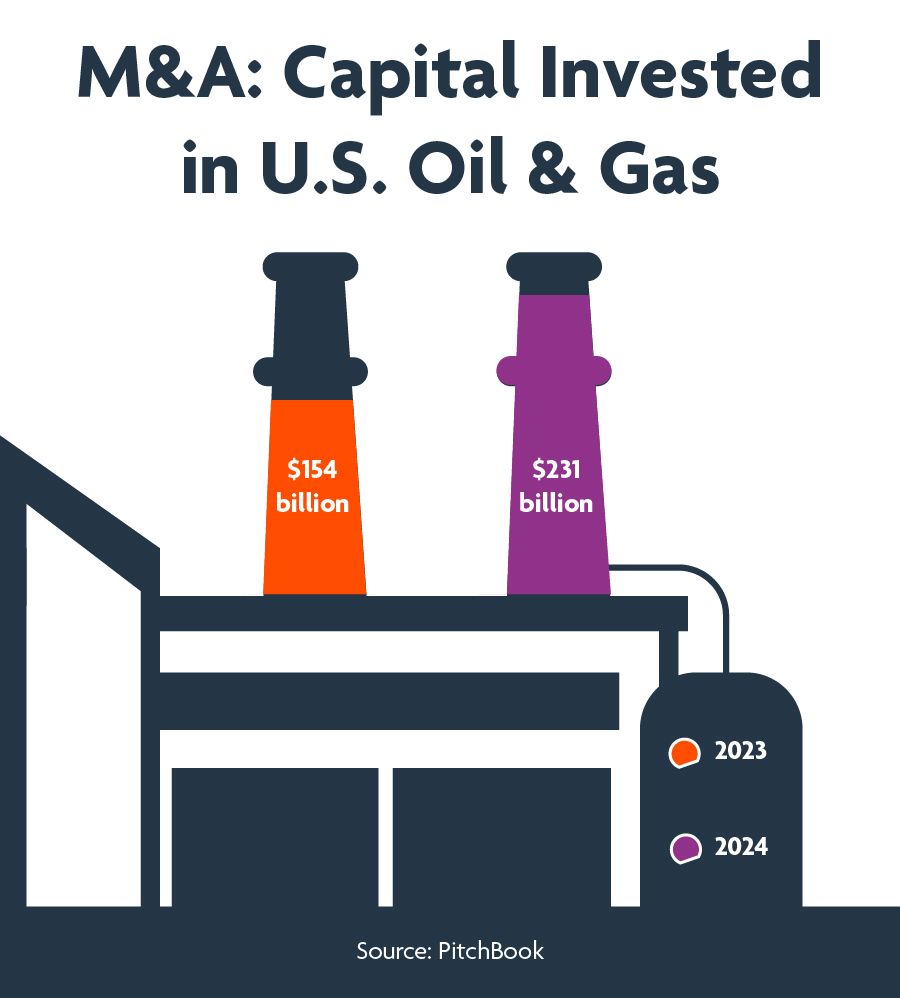

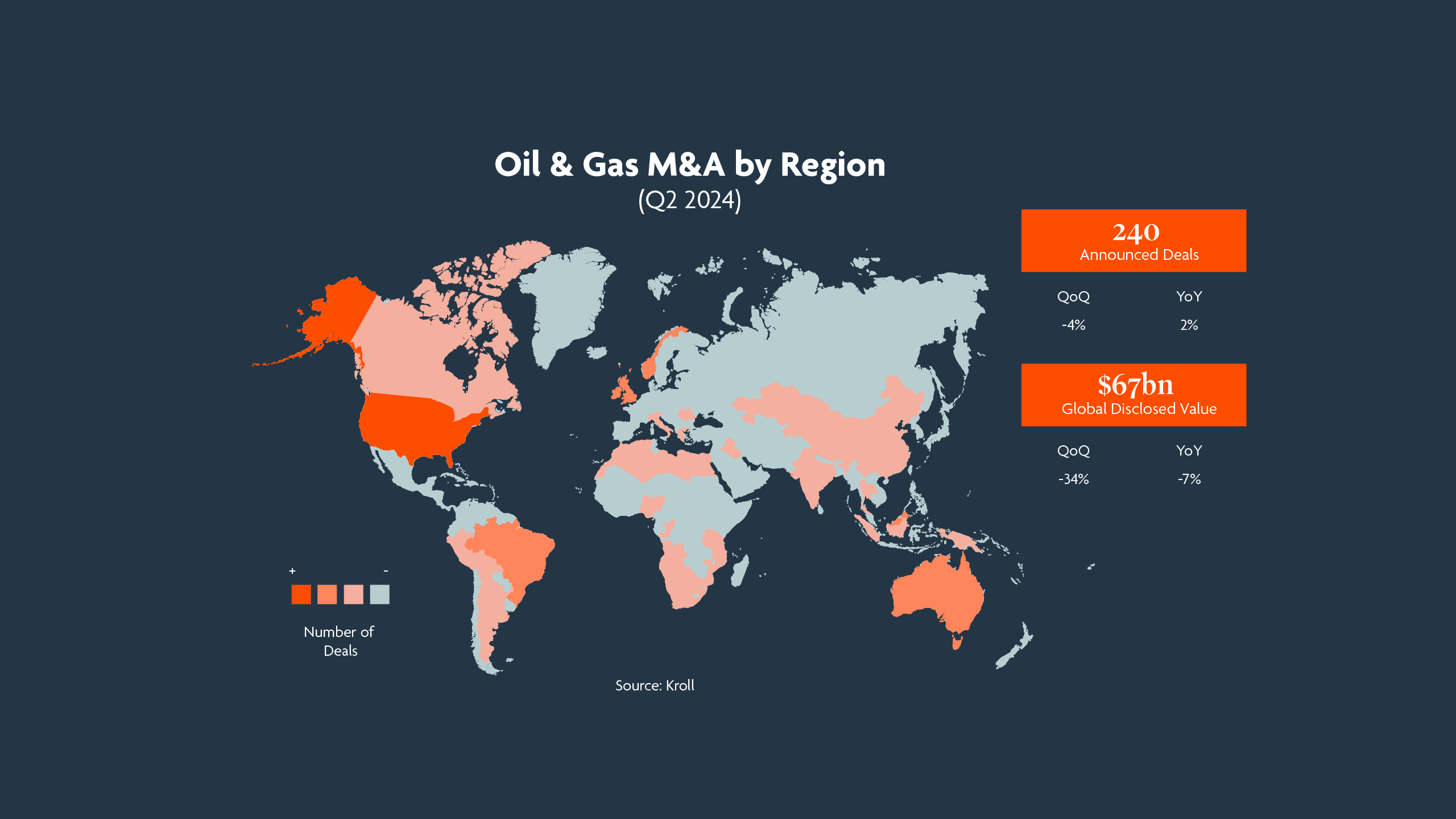

In the aftermath of those transactions, 2024 has seen fewer headline-grabbing combinations but a more consistent uptick in activity as interest rates have stabilized and access to capital has eased. PitchBook data records 2024 topping both 2022 and 2023 by capital invested, with total deal value of $231 billion up 50% on the $154 billion spent in the previous year (noting that the Exxon/Pioneer transaction was consummated in 2024 and therefore fell into that year’s numbers).

Post-Merger Rationalization Drives Asset Sales

Just two transactions valued north of $10 billion were announced through 2024 globally, with Diamondback Energy paying $26 billion for Endeavor Energy Resources to create a leading operator focused on the Permian Basin and ConocoPhillips winning shareholder approval in August for its all-stock $22.5 billion takeover of Marathon Oil. Both transactions are primarily focused on the U.S. unconventional asset market.

From a deal volume perspective, 2024 looks set to close out in line with the two prior years with around 550 oil & gas deals taking place globally. On the strategic side, much of the M&A taking place now are consolidation plays or post-consolidation asset rationalizations, as public companies look to shed what they view as noncore assets. We expect a number of the larger oil & gas players to start marketing noncore businesses in 2025.

Midstream Players Seek Their Own Tie-Ups

The massive consolidation that has taken place amongst the upstream oil & gas companies has also trickled into the midstream space, as strategics in that market look to put themselves in a similar position to scale across customers. While there have been some large public mergers as those players pursue wellhead-to-water strategies, many have opted to buy up smaller private equity-backed systems (or to acquire midstream assets from upstream companies) in order to plug gaps. Public companies are buying rather than building and looking to integrate across geographies and operations, creating a hot market for private equity owners that have midstream assets coming up to exit.

We are also entering a period during which well-funded majors are looking to make strategic investments into midstream assets and as such, we expect that to drive some deal flow in the coming year.

In the aftermath of those transactions, 2024 has seen fewer headline-grabbing combinations but a more consistent uptick in activity as interest rates have stabilized and access to capital has eased. PitchBook data records 2024 topping both 2022 and 2023 by capital invested, with total deal value of $231 billion up 50% on the $154 billion spent in the previous year (noting that the Exxon/Pioneer transaction was consummated in 2024 and therefore fell into that year’s numbers).

Post-Merger Rationalization Drives Asset Sales

Just two transactions valued north of $10 billion were announced through 2024 globally, with Diamondback Energy paying $26 billion for Endeavor Energy Resources to create a leading operator focused on the Permian Basin and ConocoPhillips winning shareholder approval in August for its all-stock $22.5 billion takeover of Marathon Oil. Both transactions are primarily focused on the U.S. unconventional asset market.

From a deal volume perspective, 2024 looks set to close out in line with the two prior years with around 550 oil & gas deals taking place globally. On the strategic side, much of the M&A taking place now are consolidation plays or post-consolidation asset rationalizations, as public companies look to shed what they view as noncore assets. We expect a number of the larger oil & gas players to start marketing noncore businesses in 2025.

Midstream Players Seek Their Own Tie-Ups

The massive consolidation that has taken place amongst the upstream oil & gas companies has also trickled into the midstream space, as strategics in that market look to put themselves in a similar position to scale across customers. While there have been some large public mergers as those players pursue wellhead-to-water strategies, many have opted to buy up smaller private equity-backed systems (or to acquire midstream assets from upstream companies) in order to plug gaps. Public companies are buying rather than building and looking to integrate across geographies and operations, creating a hot market for private equity owners that have midstream assets coming up to exit.

We are also entering a period during which well-funded majors are looking to make strategic investments into midstream assets and as such, we expect that to drive some deal flow in the coming year.

Michael Casey, head of midstream and downstream at Wells Fargo, says: “Some of the deals we’ve started to see are midsize public companies where the management teams are realizing they have carried the ball as far as they can on their own.” Greater scale will allow midstream players to deliver more, he adds:

Portfolio Diversification as a Deal Driver

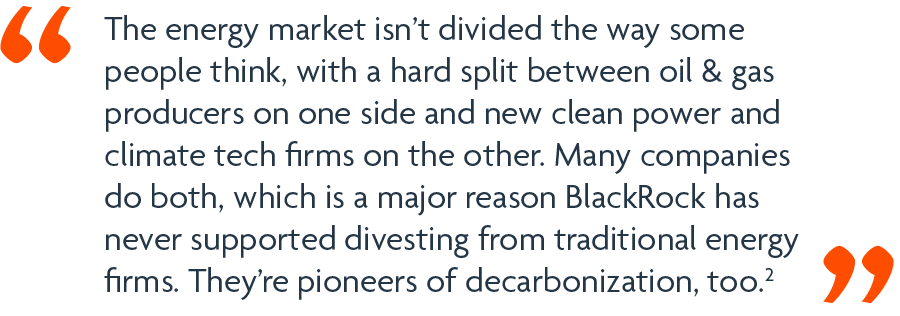

In addition to rationalization plays, supermajors have continued to diversify their portfolios of energy assets, pursuing energy transition targets to help them achieve aggressive net zero goals. It is unclear whether this will continue to be the case, given the questionable profitability of many nonhydrocarbon assets thus far. If supermajors continue down this path, then the conventional assets that they retain in their portfolios will need to be even more profitable, driving divestment of more marginal, less profitable businesses. We therefore anticipate one of two paths: either a doubling down on key assets alongside appetite for energy transition targets, or a recalculation of whether those targets are necessary or feasible.

Michael Casey, head of midstream and downstream at Wells Fargo, says: “Some of the deals we’ve started to see are midsize public companies where the management teams are realizing they have carried the ball as far as they can on their own.” Greater scale will allow midstream players to deliver more, he adds:

Portfolio Diversification as a Deal Driver

In addition to rationalization plays, supermajors have continued to diversify their portfolios of energy assets, pursuing energy transition targets to help them achieve aggressive net zero goals. It is unclear whether this will continue to be the case, given the questionable profitability of many nonhydrocarbon assets thus far. If supermajors continue down this path, then the conventional assets that they retain in their portfolios will need to be even more profitable, driving divestment of more marginal, less profitable businesses. We therefore anticipate one of two paths: either a doubling down on key assets alongside appetite for energy transition targets, or a recalculation of whether those targets are necessary or feasible.

Larry Fink, CEO of BlackRock, says:

Cash-Rich European Majors Look To Diversify

Alongside an anticipated uptick in U.S. domestic onshore M&A activity, we continue to see a fair amount of deal flow in Europe and elsewhere. Both the European majors and trading houses still have a lot of cash available to spend and national oil & gas companies continue to look for routes to diversification outside of their home markets. That has not necessarily resulted in huge deals yet, but we see the state-owned players on lots of deals chasing overseas assets and we expect them to be more acquisitive moving forward.

Larry Fink, CEO of BlackRock, says:

Cash-Rich European Majors Look To Diversify

Alongside an anticipated uptick in U.S. domestic onshore M&A activity, we continue to see a fair amount of deal flow in Europe and elsewhere. Both the European majors and trading houses still have a lot of cash available to spend and national oil & gas companies continue to look for routes to diversification outside of their home markets. That has not necessarily resulted in huge deals yet, but we see the state-owned players on lots of deals chasing overseas assets and we expect them to be more acquisitive moving forward.

Gulf Producers Pursue Acquisition Strategies

In the Middle East, too, the established regional oil & gas companies are looking to expand globally and shift their focus from being traditional domestic upstream producers into more globally integrated energy conglomerates spanning multiple verticals. These players are looking to lead deals rather than participate as co-investors and will only consider minority stakes where there is a path to control in order to drive global operational efficiencies. Given their appetite for transformation is considered time-critical, that deal activity has proved fairly resilient to market forces of late and we expect it to remain buoyant going into 2025.

U.S. Antitrust and National Security Paradigms Set to Move

Through the past 12 months, antitrust has proven to be a major variable in oil & gas M&A. There seems little doubt that the Trump administration will take a different antitrust approach, which will result in increased deal volume. For overseas investors looking to U.S. targets, strategic investments could face increased risk under Committee on Foreign Investment in the United States (CFIUS) if the administration moves to a more protectionist direction.

Gulf Producers Pursue Acquisition Strategies

In the Middle East, too, the established regional oil & gas companies are looking to expand globally and shift their focus from being traditional domestic upstream producers into more globally integrated energy conglomerates spanning multiple verticals. These players are looking to lead deals rather than participate as co-investors and will only consider minority stakes where there is a path to control in order to drive global operational efficiencies. Given their appetite for transformation is considered time-critical, that deal activity has proved fairly resilient to market forces of late and we expect it to remain buoyant going into 2025.

U.S. Antitrust and National Security Paradigms Set to Move

Through the past 12 months, antitrust has proven to be a major variable in oil & gas M&A. There seems little doubt that the Trump administration will take a different antitrust approach, which will result in increased deal volume. For overseas investors looking to U.S. targets, strategic investments could face increased risk under Committee on Foreign Investment in the United States (CFIUS) if the administration moves to a more protectionist direction.

Private Equity

Carve-out Opportunities

as Exits Tick Up

While the well-capitalized oil & gas companies continue to dominate M&A activity, we see growing opportunities for private capital to do deals.

Divestments Create Dealflow for Private Equity

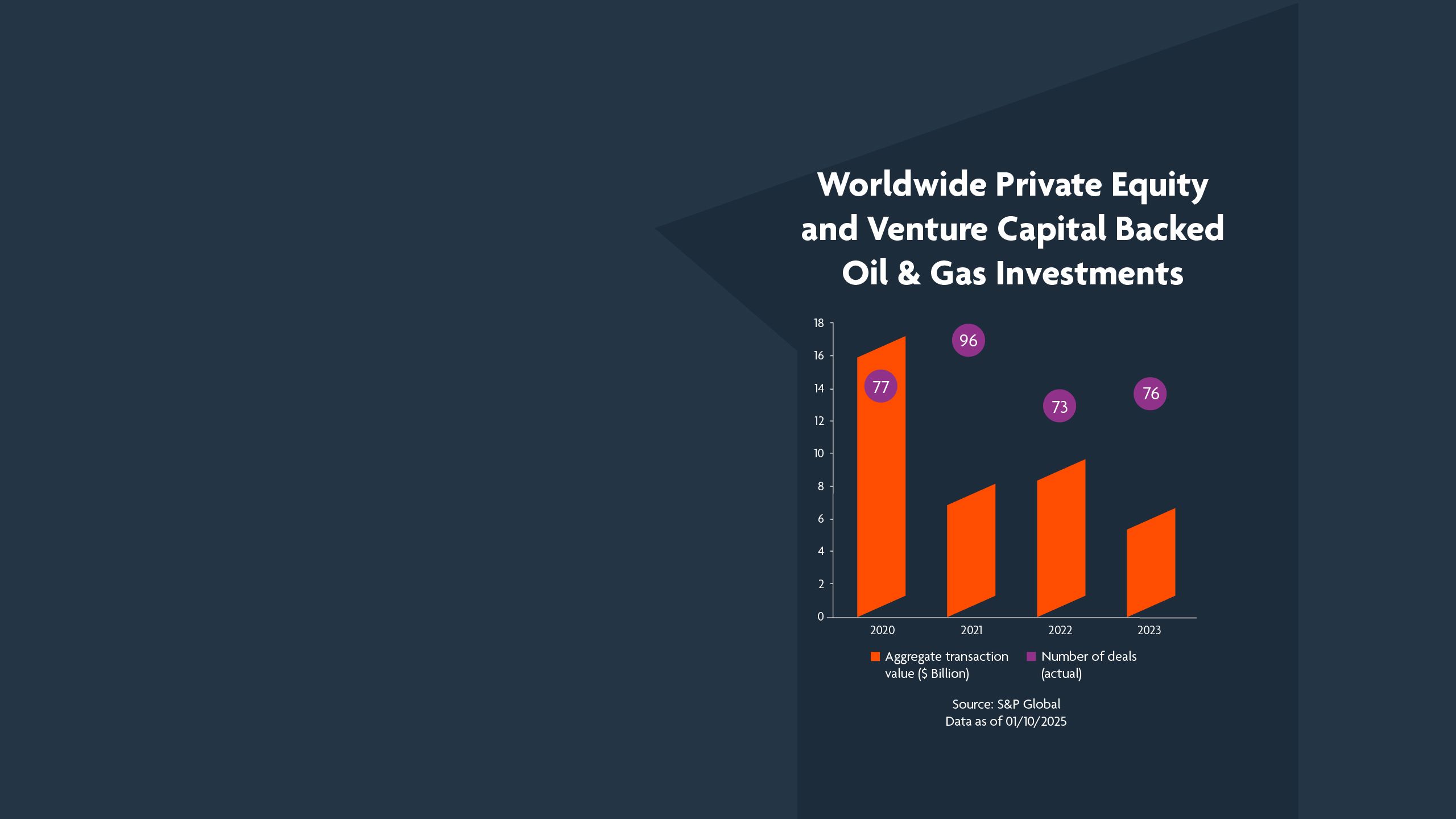

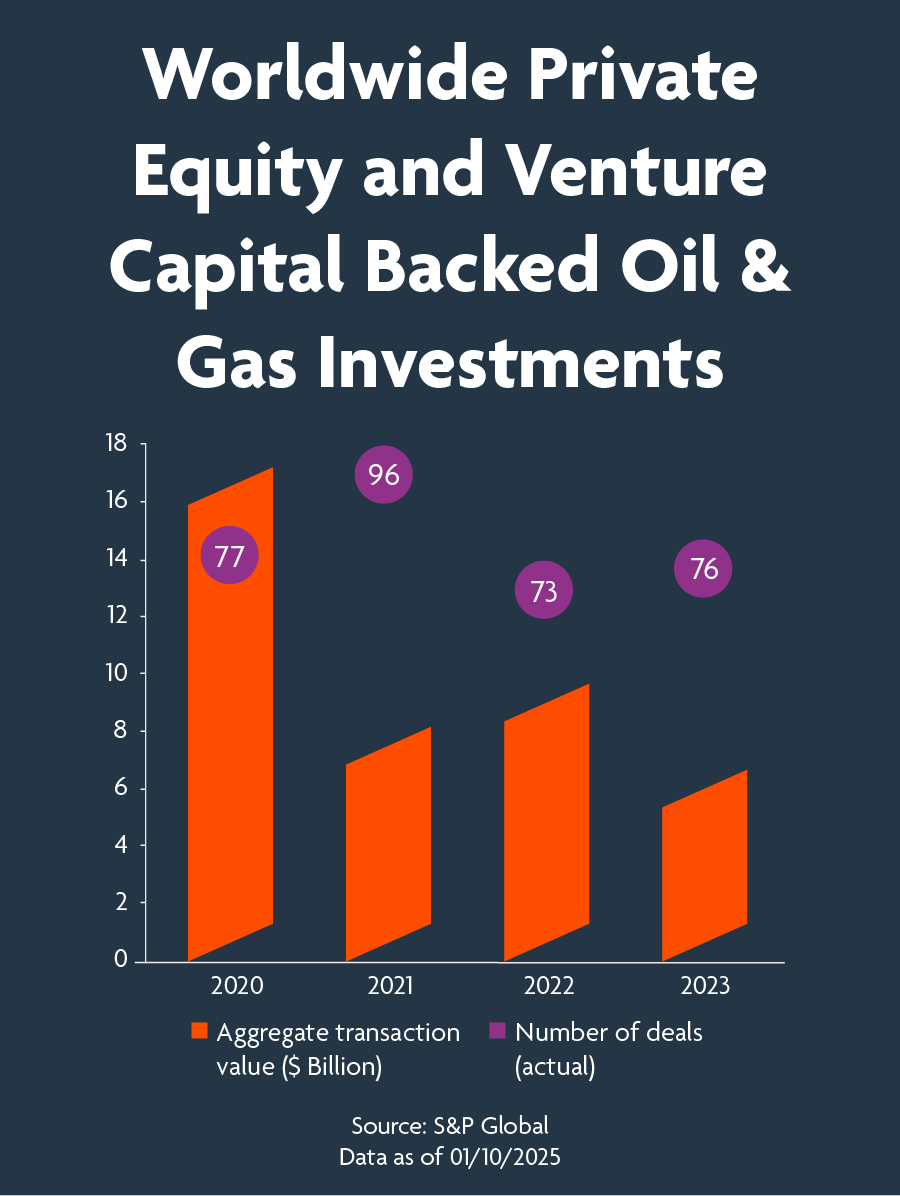

Many private equity players have raised sizeable pools of capital for energy transition in recent years, but their core hydrocarbon-focused funds were at least as busy, if not busier, during 2024. With divestments a key theme for the majors going into this year, we should see PE buyers pick up traditional assets being divested by strategics looking to rationalize.

Sponsors Line Up More Exits

On the buyside, we see an increased willingness from sponsors to take on public company equity as a proportion of the consideration for assets being sold, which is helping to get deals over the line. Across the market, private equity funds have struggled with the tough exit environment over the past 12 to 18 months and as such it feels like they are more likely to be sellers than buyers at least for the first part of 2025.

Private Equity

Carve-out Opportunities

as Exits Tick Up

While the well-capitalized oil & gas companies continue to dominate M&A activity, we see growing opportunities for private capital to do deals.

Divestments Create Dealflow for Private Equity

Many private equity players have raised sizeable pools of capital for energy transition in recent years, but their core hydrocarbon-focused funds were at least as busy, if not busier, during 2024. With divestments a key theme for the majors going into this year, we should see PE buyers pick up traditional assets being divested by strategics looking to rationalize.

Sponsors Line Up More Exits

On the buyside, we see an increased willingness from sponsors to take on public company equity as a proportion of the consideration for assets being sold, which is helping to get deals over the line. Across the market, private equity funds have struggled with the tough exit environment over the past 12 to 18 months and as such it feels like they are more likely to be sellers than buyers at least for the first part of 2025.

Joint Ventures

Energy Transition Drives Collaboration Plays

We continue to see joint ventures being discussed in the midstream and downstream parts of the market, as well as in energy transition where industry players are looking to get involved in various ways. So far, there is a lot more joint venture activity being discussed than actually getting done, and they accounted for just 32 of the 392 oil & gas deals recorded by PitchBook globally in 2024.

Partnerships Find Favor as Energy Transition Play

We are seeing a growing number of joint ventures entered into in the new energy space for large-scale hydrogen and ammonia projects, for example, where there are few single players with the scale and capabilities to move forward alone.

As we move into a new year, we anticipate more three- or four-way joint ventures being signed to bring together traditional oil & gas players on the supply side, renewables developers and off-takers in order to get projects off the ground. A case in point is the NEOM Green Hydrogen Project in Saudi Arabia, which is the world’s largest utility scale, commercially based hydrogen facility powered entirely by renewable energy, structured as an equal joint venture between NEOM, Air Products and ACWA Power.

Joint Ventures Will Likely Connect Hydrocarbon and Power Players As Well

A number of power generators and large-scale power users (e.g., data centers and other technology players) have seen the coming need for reliable power and are exploring the use of the large U.S. supply of natural gas to this end, as well as potential use of smaller modular nuclear reactors. We expect to see a number of joint ventures or other strategic arrangements in these spaces in the Permian Basin and elsewhere in North America.

More Combinations in the Gulf To Fuel Domestic Growth

In the Middle East, a flurry of domestically focused joint ventures has been driven by a desire to bring in strategic international partners in order to drive domestic growth. While those deals have been far outpaced by an appetite for international investment, we have sometimes seen them in conjunction with an equity investment where there will be a domestic component driven by the target establishing a local joint venture.

Joint Ventures Work for Midstream Strategies

We also expect to see more joint ventures entered into among midstream businesses as those look to collaborate in order to provide that wellhead-to-water solution for their customers.

Joint Ventures

Energy Transition Drives Collaboration Plays

We continue to see joint ventures being discussed in the midstream and downstream parts of the market, as well as in energy transition where industry players are looking to get involved in various ways. So far, there is a lot more joint venture activity being discussed than actually getting done, and they accounted for just 32 of the 392 oil & gas deals recorded by PitchBook globally in 2024.

Partnerships Find Favor as Energy Transition Play

We are seeing a growing number of joint ventures entered into in the new energy space for large-scale hydrogen and ammonia projects, for example, where there are few single players with the scale and capabilities to move forward alone.

As we move into a new year, we anticipate more three- or four-way joint ventures being signed to bring together traditional oil & gas players on the supply side, renewables developers and off-takers in order to get projects off the ground. A case in point is the NEOM Green Hydrogen Project in Saudi Arabia, which is the world’s largest utility scale, commercially based hydrogen facility powered entirely by renewable energy, structured as an equal joint venture between NEOM, Air Products and ACWA Power.

Joint Ventures Will Likely Connect Hydrocarbon and Power Players As Well

A number of power generators and large-scale power users (e.g., data centers and other technology players) have seen the coming need for reliable power and are exploring the use of the large U.S. supply of natural gas to this end, as well as potential use of smaller modular nuclear reactors. We expect to see a number of joint ventures or other strategic arrangements in these spaces in the Permian Basin and elsewhere in North America.

More Combinations in the Gulf To Fuel Domestic Growth

In the Middle East, a flurry of domestically focused joint ventures has been driven by a desire to bring in strategic international partners in order to drive domestic growth. While those deals have been far outpaced by an appetite for international investment, we have sometimes seen them in conjunction with an equity investment where there will be a domestic component driven by the target establishing a local joint venture.

Joint Ventures Work for Midstream Strategies

We also expect to see more joint ventures entered into among midstream businesses as those look to collaborate in order to provide that wellhead-to-water solution for their customers.

Conclusion

Fewer Mega-deals

But a Busy Year Ahead

While 2025 is expected to be an active year for M&A, it will be a little different than the last year of heightened M&A activity.

With a new president in the White House and elections settled in major countries around the globe last year, more stable interest rates and greater visibility should strengthen deal flow in the year ahead, but we expect an uptick in volume of mid-market deals to replace the mega-transactions of a year ago.

As the industry continues to navigate a shift in oil demand that is pushing the majors to rationalize and hone in on their most profitable business lines, 2025 activity will be characterized by opportunistic acquisitions of noncore assets coming off the back of a consolidation wave.

1 See https://www.reuters.com/business/energy/ceraweek-us-pipeline-firms-poised-follow-biggest-customers-into-ma-2024-03-21/

2 See https://www.blackrock.com/corporate/investor-relations/larry-fink-annual-chairmans-letter

Conclusion

Fewer Mega-deals

But a Busy Year Ahead

While 2025 is expected to be an active year for M&A, it will be a little different than the last year of heightened M&A activity.

With a new president in the White House and elections settled in major countries around the globe last year, more stable interest rates and greater visibility should strengthen deal flow in the year ahead, but we expect an uptick in volume of mid-market deals to replace the mega-transactions of a year ago.

As the industry continues to navigate a shift in oil demand that is pushing the majors to rationalize and hone in on their most profitable business lines, 2025 activity will be characterized by opportunistic acquisitions of noncore assets coming off the back of a consolidation wave.

1 See https://www.reuters.com/business/energy/ceraweek-us-pipeline-firms-poised-follow-biggest-customers-into-ma-2024-03-21/

2 See https://www.blackrock.com/corporate/investor-relations/larry-fink-annual-chairmans-letter